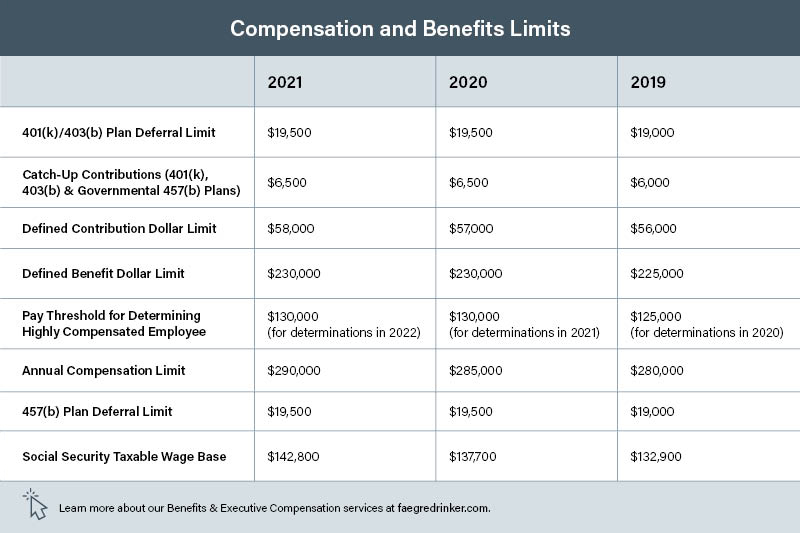

The Internal Revenue Service (IRS) recently announced the 2025 cost-of-living adjustments to various benefit and contribution limits applicable to retirement plans. The IRS modestly increased the applicable limits for 2025. The following limits apply to retirement plans in 2025:

- The limit on elective deferrals under 401(k), 403(b) and eligible 457(b) plans increased to $23,500.

- The limit on catch-up contributions by participants aged 50 or older did not change and remains at $7,500. This means that the maximum amount of elective deferral contributions for those participants in 2025 is $31,000.

- The enhanced catch-up contribution limit for those ages 60-63 in 2025 is $11,250. This means that the maximum amount of elective deferral contributions for these participants in 2025 is $34,750.

- The Internal Revenue Code (Code) Section 415 annual addition limit is increased to $70,000 for 401(k) and other defined contribution plans, and the annual benefit limit is increased to $280,000 for defined benefit plans.

- The limit on the annual compensation that can be taken into account by qualified plans under Code Section 417 is increased to $350,000.

- The dollar level threshold for becoming a highly compensated employee under Code Section 414(q) increased to $160,000 (which, under the look-back rule, applies to HCE determinations in 2026 based on compensation paid in 2025).

- The dollar level threshold for becoming a “key employee” in a top-heavy plan under Code Section 416(i)(1) is increased to $230,000.

Continue reading “IRS Announces 2025 Retirement Plan Limits”